|

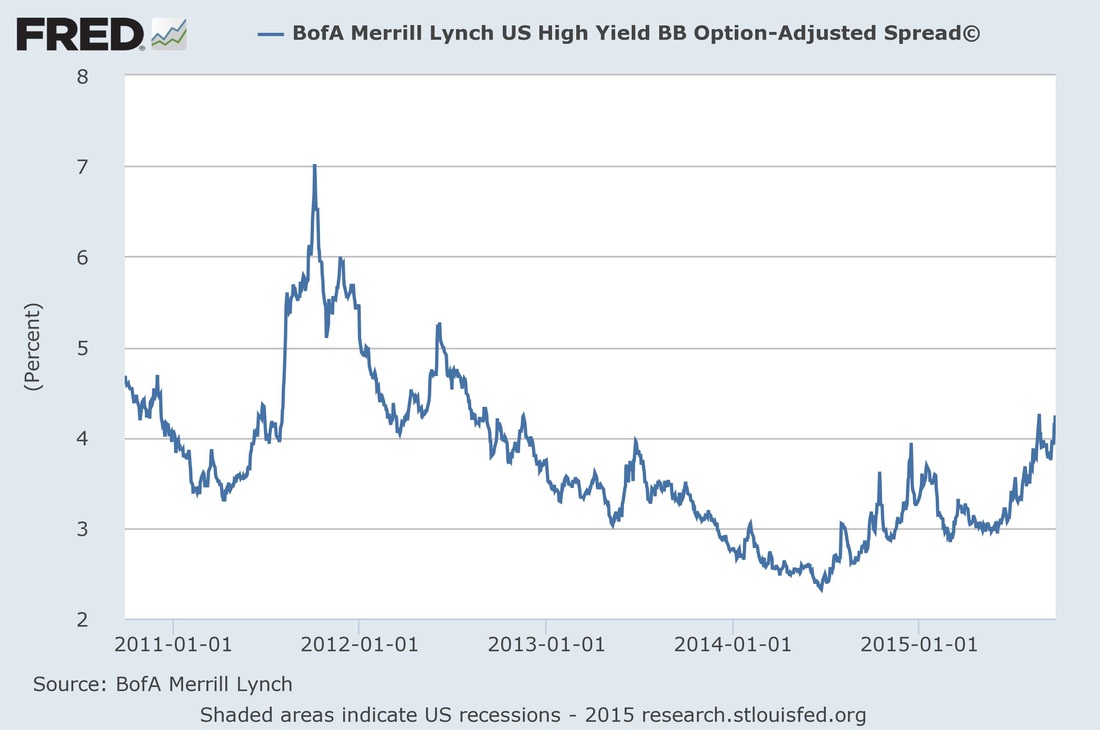

“In theory there is no difference between theory and practice. In practice there is.” – Yogi Berra Yogi Berra passed away last week. He was a writer’s dream, providing me with great quotes over the years. Plus he was my grandma’s favorite player, so that counts for a lot. He will be missed. This week’s letter is a little late due to some outside events. Literally outside. It’s grape harvest time in the Columbia River Gorge and as the owner of a vineyard, it’s all hands on deck over here. The kids are taken out of school, given clippers and a bucket, and get to learn what it means to do real work. Then last night we spent a few hours watching the lunar eclipse from the Rose Garden in Washington Square Park in Portland under a cloudless sky. I hear it was cloudy in a lot of the country, but at this time of the year in the Pacific Northwest it’s usually crystal clear, and last night was no exception. Family first… I had a plan all week to write about actual stocks. Not the Fed, not interest rates, not macro stuff. Just a few stocks. And then the market fell 2.5% today and I had to scrap that plan, but I’m still going to talk stocks, just different ones than initially planned. The others are getting moved to our StockPicker newsletter instead. Email me for a free trial. In theory, issues affecting other markets, or sectors that are peripheral to our markets, shouldn’t knock down the whole U.S. stock market 2.5% in a day. But they did. And I think they will continue to have an impact for a little while longer for a few reasons. Right now, cars, credit, and commodities are creating some more of those nasty correlations we have been talking about lately. The cars in the title are Volkswagen. VW isn’t a part of U.S. indices, but it is a huge part of the German market, and along with other German carmakers (Daimler, BMW) and their suppliers accounts for nearly 775,000 jobs and 20% of all German exports. VW is the new Greece for the German economy. One company’s scandal won’t cause a recession, but the issues dogging the company have made the DAX fairly uninvestable at the moment. This isn’t good for global funds that thought Germany was the safe haven in Europe. And we know what happens when global macro funds get hit in one market – they sell in all of them. "A nickel ain't worth a dime anymore." – Yogi Berra Credit and commodities are linked. Oil and copper and other commodities are in a free-fall, creating problems for companies that borrowed a lot to build the capacity to mine or drill for them. High yield spreads (see the chart below) are widening out. This creates problems for investors who lent at very low spreads last year, when a record amount of debt was issued. Now add in the unfolding saga at Glencore. The correlation here is from potential counterparty risk if Glencore gets downgraded to junk. Risk resides somewhere – but the question is where and in what form. Glencore is a big borrower ($26 billion comes due in the first half of 2016) and its credit default swaps are blowing out to extreme levels. My inbox has a number of reports on what banks have exposure to Glencore debt, which is never a good sign for the company in question. However, this is not just a Glencore problem -- high yield spreads overall are widening (albeit from very low levels), and new deals are coming below par with higher-than-marketed spreads. As usual, high yield was the canary in the coal mine for the stock market – spreads started widening in late June. The new capital given to the oil industry earlier this year was banking on a recovery in oil prices – and when oil prices fell over the summer instead of sustaining their rebound, credit markets got more realistic about the industry’s prospects.  "Nobody goes there anymore. It's too crowded." – Yogi Berra So what is different today that hasn’t been known to the markets for a few months? Commodities have been terrible for awhile. Glencore has been in the news for weeks. Energy is about 7% of the S&P 500 and Materials are under 3%. Well, today the markets got word that Hilary Clinton’s tweet from last week about price-gouging in drug prices (after Turing’s CEO did a star turn as the douche-bag CEO of the year), which wrecked biotech stocks, has now gone viral, as House Democrats asked to subpoena Valeant for documents related to drug price increases. Valeant was off over 12% today, and 4 other pharma companies stocks fell more than 10%. This healthcare selloff is what caused the most pain in the markets today, as U.S. stock fund managers have more exposure to healthcare than to materials and energy combined. Pharma was the place fund managers could hide – there was a lot of M&A, companies had activists backing them, borrowing for deals was cheap. Now M&A is in doubt, as the industry has apparently become the new whipping boy for Congress. (Does this mean the banks are now finally out of the hot seat? If so, they’re cheap…). Healthcare is a very crowded trade. Suddenly, with all this risk, nobody goes there anymore… "The future ain't what it used to be." – Yogi Berra This is where those nasty correlations come into play again. High yield has always been a leading indicator for equity markets for me – high yield spreads widening imply that equity risk premiums are also likely to increase. High yield spreads widened on energy worries late last year, but then tightened again as companies issued equity and refinanced debt. However, the most recent spread increase has coincided with bigger worries about global financial markets overall. If you were a simple stock fund that sensibly avoided all this mess by staying away from energy and commodities, you may well have been hiding in the “safe” auto and healthcare industries. Which is what makes the car problem and Clinton problem big problems – they are hitting stock investors where it hurts. J.P. Morgan said it well in a note today: “HC isn’t just big (~15% of the SPX) but has also been a massive contributor to fund performance over the last 1-2 years (thus the HC stock plunge has inflicted enormous amounts of P&L pain throughout the fund community and that is only adding to the broader risk-off trend).” "If people don't want to come out to the park, nobody's going to stop them." – Yogi Berra I think investors feel under siege. Global macro players have been hit by emerging market and currency volatility, global bond investors have been hit by credit spreads widening, and now stock investors are being hit in what they thought were their safe havens too. Buyers who were patient and added to their favorite stocks on the recent pullbacks are now sitting on losses on almost all of those buys. If you had a plan to buy a position in thirds, and you bought your first third on the first drop and the second third last week, well, now you’re looking at your book and thinking “do I really need to buy those last shares here? Why not wait a few days and see what happens?” Buying the dips, unless you were really good on August 24th, means you’re starting to feel some pain. (See the SPY chart below). And the thing about the stock market is, if you don’t want to come out to the park, nobody is going to stop you.  This week’s Trading Rules:

Resistance: 192, 195, a lot at 197/199, then 201 and 205. Positions: Long and short U.S. stocks and options, Long SPY Puts. For more ideas, charts, and market information, Email me for a free trial of my bi-weekly StockPicker newsletter. No credit card or other financial information is required. Comments are closed.

|

Archives

March 2023

Categories |

RSS Feed

RSS Feed