|

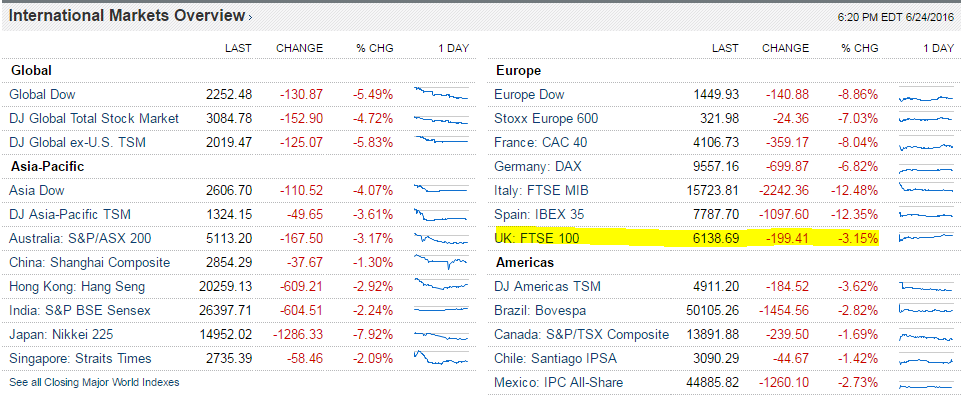

Boys, I got myself a pretty good bullshit detector, and I can tell when somebody's peeing on my boots and telling me it's a rainstorm. Ed Earl, The Best Little Whorehouse in Texas As you may have heard, the British decided to have their own Independence Day on Thursday. “Leave” voters are being derided by the press and the losing side as ignorant, foolish, intolerant, xenophobic – and those are the nice things. I call B.S. The Leave voters are none of these things. They are just tired of being told that the EU is going to save them, when in reality most of the issues in the EU economies can be chalked up to an over-reaching regulatory state. The EU isn’t working. The economies in it have been eviscerated over the past decade by the very institutions that the Remain people are now saying Britain needs. Needs why? As I heard one hardworking gentlemen state on BBC World News today (I know he’s hard working because he was interviewed while literally unloading a truck – how many of the posh bureaucrats in Brussels have ever worked a truck you think?) – “Great Britain has been around for a very, very long time, and we’ll be just fine.” Good for him – he’s right. Am I saying that Brexit won’t have an impact on the British economy? No. I’m saying I don’t know what the impact will be, but staying in the EU wasn’t going to be good. So after a long period of being tied to stagnating, at best, economies on the Continent, leaving to give it a go on their own isn’t so crazy. Think about it. The EU is a morass of poor performing economies – some of the worst in the world – led by career bureaucrats who think that the answer to every problem is more regulation, more government, more centralization of power, more Central Bank meddling in the economy. And despite the fact that it has produced absolutely horrible growth (if there is any real growth at all), despite the fact that innovation outside of a few Nordic countries is basically non-existent in the EU (can someone point me to their Silicon Valley? No? Didn’t think so), despite the fact that the ECB has had to push rates negative across Europe in a blind leap of faith that maybe that will work where nothing else has, despite all this, it’s just crazy for Britain to say, eh, screw it, we’ll give this a try on our own. Who’s the crazy one? I’d say all those folks crying wolf that the EU is the only alternative. Because piss ain’t rain. Don't feel sorry for me. I started out poor, and I worked my way up to outcast. Miss Mona, The Best Little Whorehouse in Texas Oh, by the way, did you notice that the “uneducated masses” who voted for Leave managed to do what the “genius” PH.D.s running the central banks in Japan and Brussels have been trying to do for years without success? They devalued their currency, and didn’t tank their stock market. That’s right, the “crash” in the Sterling (and Sterling is just back to where it was on February 26, 2016 by the way) is exactly what Draghi and Aso have been trying without success to do to the Euro and the Yen. When they do it, it’s called monetary policy. When the Leave campaign does it, it’s called a disaster. Okey dokey. Want to know which major stock market performed the best on Friday? (Asian markets closed before Leave vote was confirmed.) Great Britain’s. And it was up on the week. Nice trick, that. So despite all the wailing about how this will be a disaster for Britain, the people who actually have to bet with their money disagree. I’d follow the money.  They want me to close her down, run her out of town. How can I ask her to leave when all I want her to do is stay? Ed Earl, The Best Little Whorehouse in Texas In fact, if you follow the money, Brexit isn’t bad for Britain – it’s bad for the EU. Check out those Italian and Spanish returns – they are the worst one day returns in the history of their markets. Apparently, some folks were expecting the British to take on some of the problems of Italy and Spain. Quoting Spiro Agnew, the “nattering nabobs of negativism” are talking their book – which is long all the bad loans on the Continent. Economically speaking, outside of losing some, but nowhere near all, finance jobs that must be done within the EU per regulation, this will prove to be a net benefit in the long run for Britain. It’s getting rid of the dead weight that is dragging down all the economies of the EU. It’s putting behind it the stagnation and regulation that’s killing innovation. One of the arguments for Remain was that leaving will require the unanimous agreement of the other 27 countries to any of the terms. I’d say that’s a great argument for Leave… What are three of the strongest countries in Europe? Norway, Iceland, and Switzerland (you can throw in Liechtenstein if you want as well). None are in the EU. Now I’m not saying there won’t be some issues to work out. Visa-free travel and the freedom to work anywhere in the EU were nice – but also part of the problem. At the end of the day, more than half of the British people decided that you know what, I don’t travel that much, and I want to stay and work in the town where I live now, so those things aren’t that important to me. They are important to the two groups that mainly voted to Remain – the young, and the international set in London. If you’re used to hopping over to Paris for a quick meeting, going through customs will be a bit of a drag. Welcome to the rest of the world. If you’re young and were hoping to spend a few years just roaming around the continent, working a bit here, loafing a bit there, well, you can’t anymore, and that sucks. But that’s the way democracy works sometimes, and lots of folks decided that unrestrained immigration from the Middle East wasn’t a thing they wanted to support. Besides, Britain never really wanted to be a part of the EU in the first place. Just watch this video for (funny) proof. The border between Ireland and Northern Ireland will be an issue. Right now, it’s open border, but not long ago it was a militarized flash point that cost many, many lives. Going back to that won’t be good, and solving the Irish issue won’t be easy. To me, this is the biggest looming problem from a societal standpoint, and I’m not sure what the right solution will be. Belfast is still a divided place, and could quickly devolve into violence. Hope isn’t a strategy, but it’s all we have there at the moment. Ed Earl, I think the best thing to do is to put this behind us, just as quick as we can. I've made a little money, I've laughed some, I've danced to the music…it's just time to pay the fiddler, that's all. Miss Mona, The Best Little Whorehouse in Texas So back to the markets, which is the focus of this letter. In the U.S., the SPX closed right on its lows (it traded lower Thursday night, but not during the daytime session), but the session was fairly devoid of panic until the closing minutes. Trader lore is that markets never bottom on a Friday, as investors have all weekend to read the worried cognoscenti’s dire predictions (tip: ignore them). Markets usually start to put in a bottom on the morning of day 3 after a shock, as that’s when forced sellers (aka, those with margin calls) and those who invest via model portfolios get out. Technically, stocks behaved as expected – the SPY bounced right off the support we noted in our last letter at 204/205, before breaking down at the end of the day and settling at 202. There is a little support about 1% lower at 200, but if we follow the risk-off playbook from January we could be heading back to 190 over the next week and 185 if things get ugly. For now, I’d continue to play defense and stay well hedged. In the last letter, I said “Lots of smart investors are saying markets are at unsustainably high levels and are preparing for a selloff. Bill Gross warned of a bond market “supernova”. Soros is taking down his firm’s equity exposure and buying gold. Same for Druckenmiller. At John Mauldin’s recent Strategic Investor Conference, the speakers were almost all uniformly bearish.” Turns out they might be right. This selloff is pretty minor so far for the overall market – we’re just back to where we were in mid-May. But I don’t think it’s over just yet. If you’re inclined to go shopping, I’d look at the U.S. regional banks, which have been just crushed – some were down over 10% on Friday alone, despite having zero exposure to Europe. The ones down the most suffer from a combination of asset sensitivity (they make more money when rates are higher) and exposure to oil. The outlook for both is now lower for longer, as the strong dollar makes raising rates difficult for the Fed, and the strong dollar makes oil cheaper here in the U.S. So the flight to safety trade by macro funds has hit the smaller regional banks in the Western United States. Welcome to investing, circa 2016. We’re all connected. And we’re not even in the EU. __________________________________________________________________________ This week’s Trading Rules are repeats, since they are appropriate in this environment:

The broader market has been performing worse than the S&P 500, as utilities and staples hold up the index. Tech and financials have been especially weak lately. I’d go shopping there for bargains if you have a time frame longer than a week. Financials are being hurt by the prospect of “lower for longer” again in the U.S. and weirdness from negative rates abroad. Tech is being hurt by weak global growth outlooks, but the best businesses will be fine, especially those with a U.S. focus. SPY Trading Levels: The market was coloring within the lines until Friday. The SPY stopped just at the big resistance level of 209/210 before the Friday fall. Resistance is now 206, 208, 210 and 212. Lots of overhead. Support: small at 202 and 200, a decent amount at 194/195, then 188/190. After that 184/185. Positions: Long and short U.S. stocks, ETFs and options. Neutral stock exposure, net short down 1%. Yes, and how many years can a mountain exist

Before it's washed to the sea? Bob Dylan, Blowin’ In the Wind There is a mountain of overvalued debt in the world, and folks are beginning to wonder how long it can exist before it washes out to sea. About $8 trillion in debt around the world is currently trading at a negative interest rate, implying that the holders of this debt expect deflation for the foreseeable future. Smart, rational investors around the world are bemoaning the stupidity of this situation in increasing numbers, but central bankers push onward with their quest to drive rates even lower, in the hope (wrongly) that lower rates will spur lending by banks and investing by companies. Yes, you read that right – the geniuses in Brussels think that lower rates will make banks want to lend more. Why? Because that’s what their broken models tell them. Don’t believe me? Watch this video on the inner workings of the ECB’s bond buying operations. Skip ahead to the 2:30 mark for the explanation of why they are doing it, but be sure you’re alone, because if you actually have a brain and think about what he says, you’re going to want to scream. If you want to understand the crazy distortions in bond markets today, take 3 ½ minutes to check it out. In the U.S., the picture is a bit better, but the weak jobs report in early June took down the market’s expectations for near-term Fed rate hikes significantly. This caused financials, which had been acting well of late, to sell off this past week, as they are desperate for higher rates in order to make lending more profitable. Unfortunately, they have hordes of Ph.Ds at the Fed and ECB standing in their way. (Did you know that there are 750 Ph.Ds on the staff of the Federal Reserve alone?) These economists all follow the Keynesian theory that we have a consumption problem – ie, that consumers aren’t buying enough stuff to create scarcity and drive up inflation to their preferred target. For some reason, they think that lower rates will drive consumption, despite the fact that ultra-low rates for the past seven years have failed to do just that. They think that consumption is a borrowing-cost problem, when in reality it’s an income problem. And they are the ones that are creating it. How? By stripping massive amounts of interest income out of the economy. When the Fed buys bonds and artificially lowers interest rates below their natural market-level, they are stripping income from the economy. That 5% in interest payments that the government used to pay to savers, insurance companies and pension plans is now under 2%, and mostly paid to the Fed. What does the Fed do with its interest payments? Nothing. It simply gives it back to the Treasury. All that income is taken out of the system. Sure, some investors move on to other yield investments, which explains the overvaluation of income stocks like utilities and telecoms, but there is more uncertainty in these securities, more volatility in their prices, and therefore a lower propensity to spend the income they generate – so savers hoard their assets instead of spending the income. This explains the really low velocity of money in the U.S. economy, because when savers, like retirees in Florida, can’t earn enough income from bank CDs and Treasuries, but are forced into risky assets they really don’t want to own just to earn enough income to pay the rent and food, they aren’t going to be out there spending on anything but the basics. That new outfit? It can wait. New golf clubs? Last year’s work just fine, thanks. Fancy meals out? I’ll stay home and cook instead. So when these savers fail to spend, the Fed, and its 750 Ph.Ds, decide that well, our models show that lower rates should boost spending (how? they never explain, because it doesn’t work), so we’re going to just lower them more, or put off raising them, despite the evidence (see Japan) that low rates do not create inflation or more spending – they kill it. If you want to create more spending and monetary velocity, you need to increase consumers income. You need to get them more income today than they had yesterday, and they need to feel confident that that increase in income is safe and sustainable. Want to increase spending at restaurants in Florida? Take Fed Funds to 6% again. Want to make pension plans solvent? Take Fed Funds to 6% again. Want see banks falling all over themselves to make loans to small businesses again? Take Fed Funds to 6%. It’s simple. Don’t believe me? Give every saver with $500,000 in investable assets an additional $25,000 a year in income and see what happens. The Fed has the power to increase incomes tomorrow if it wanted, but it doesn’t really understand that. Incomes create spending, which will create the inflation they want. Don’t believe me? Give every person of working age in the U.S. one million dollars tomorrow and see what happens to inflation – there will be lines out the door of every Best Buy and auto dealer in the country. Too simple? Maybe. But directionally, that’s how it works. Unfortunately for the global economy, the inmates running they central banks insane asylums don’t get it. So what’s an investor to do in such an environment? I don’t think the sovereign debt of countries that have their own currency and an accommodative central bank (CB) is much of an issue. So long as the CBs are willing to finance the debt, and continually roll it over, then it never really needs to be repaid and taxes don’t have to be diverted from spending to pay it down. How long can this go on for? Forever. When debt comes due, the CB can just print more money, hand it to the Treasury, who gives it back to the Fed for its bonds, and voila – no more debt. Or, they just issue more debt that the CB buys, and they leave the same nominal amount outstanding. So the U.S., China, U.K., Japan and other countries with their own currencies are fine. The Eurozone countries are in a bit more precarious position, particularly because Germany doesn’t really seem to understand this mechanism and balks at “bailing out” weaker members of the currency union. For now, the ECB seems to be pushing on without them, and rolling their debt, but the restrictions Germany wants to impose on its Eurozone partners could eventually lead to further crisis. For now, however, I think that sovereign debt fears are overblown in the face of an overwhelming cover bid from CBs around the world. Corporate debt is a different animal – while the ECB is now buying corporate bonds in addition to sovereigns, its ability to roll over a bond from a distressed borrower is somewhat in question in my mind. If you have a corporate borrower that runs into issues and doesn’t have the cash flow to pay back its debts, what will the ECB do? Extend and pretend? Foreclose? How will it foreclose – it doesn’t have the systems and people in place to do it? Collecting a debt is not a simple academic exercise of asking nicely – it entails securing collateral, selling that collateral, enforcing guarantees, etc. There’s a reason why distressed debt firms get paid a lot of money – because getting your money back is hard work. Here’s where I see a problem developing. Smart investors are pointing to the 18% non-performing loan levels in Italy (which they claim are understated!) and saying this is where the next banking crisis in Europe will come from. Maybe. I’m not that smart to know. But I do know that when bad corporate debt meets an unsophisticated government buyer, bad things will happen. They always do. Yes, and how many times can a man turn his head And pretend that he just doesn't see? The answer, my friend, is blowin' in the wind Bob Dylan, Blowin’ In the Wind The global hunt for yield has created some really risky securities, which investors would do well to avoid seeing in their portfolios despite the fact that they have been some of the best performing sectors in the U.S. stock market recently. In particular, utilities, telecoms, and consumer durables stocks are trading at ridiculously high valuations, as investors try to hide in “low vol” stocks and yield plays. Unfortunately, those needing safety and income the most are the ones most at risk in this market, as these stocks are pricing in all future returns today. Quoting John Hussman’s latest letter: An extended period of modest interest rates encourages investors to forget what I often call the “Iron Law of Valuation”: the higher the price an investor pays for a given set of future cash flows, the lower the long-term investment return one can expect. With every increase in price, what was “expected future return” only a moment earlier is immediately transformed into “realized past return,” leaving less and less future return on the table. Investors over-adapt to low short-term interest rates by chasing yields and driving up the valuations of much riskier securities (mortgage securities during the housing bubble, equities, corporate debt, and covenant-lite junk securities in the current episode). The rising asset prices also convince investors that risky assets really aren’t actually risky, and a self-reinforcing bubble results. Ultimately, low interest rates aren’t followed by high investment returns at all. Rather, low interest rates encourage concurrent yield-seeking speculation for a while, but after an extended period of yield-seeking, the overvaluation is followed by awful subsequent outcomes over the completion of the market cycle. Lots of smart investors are saying markets are at unsustainably high levels and are preparing for a selloff. Bill Gross warned of a bond market “supernova”. Soros is taking down his firm’s equity exposure and buying gold. Same for Druckenmiller. At John Mauldin’s recent Strategic Investor Conference, the speakers were almost all uniformly bearish. (For an excellent recap, read Steve Blumenthal’s On My Radar – and sign up to get it every week, for free – it’s a must-read). Unfortunately, their timing can be off, especially for fund managers who are judged on a monthly basis. Investors in stock funds have become so short-term oriented in their view, in particular pension fund investors, that the managers of these funds feel great pressure to do things that they ordinarily wouldn’t do in order to “keep up appearances” for lack of a better phrase. They search for the “least bad” alternative in the hope that they can generate competitive returns in the face of overvalued markets and be able to jump off the moving merry-go-round without getting hurt. For mutual fund managers, the quarterly performance reviews and quick-triggers of fund boards will almost ensure that they maximize the pain of their investors in the next downturn, as managers that have shown conservatism and restraint have mostly been shown the door by the bull market of the past 7 years. On the rare occasions that I discuss markets socially, I feel terrible for those that don’t know any better and continue to blindly index their life savings to overvalued markets. The drumbeat of the financial press about the failings of active managers, and the focus on relative short-term performance instead of absolute performance over a full market cycle by allocators, is going to inflict some serious damage on investor’s portfolios in the next downturn. When will this downturn come? I really don’t know. So many things that could have been the spark that lights the fire have come and gone without a trace over the past 7 years, so why will this time be any different? A prudent investor in this environment will focus on idiosyncratic investments, both long and short, special situations, like spinoffs, takeover candidates, and restructuring stories that can add value without the overall market moving up. But since these investments can be crushed in a broad market decline despite excellent fundamentals, investors looking to preserve capital must hedge in this market, despite the high-cost of doing so, either via options or outright shorts. Yes, the prudent investor will underperform if the market turns and rips higher, but they will also preserve capital and be able to take advantage of the bargains that the eventual selloff will create when it finally occurs. __________________________________________________________________________ This week’s Trading Rules:

Stocks, especially small caps, pushed higher the past few weeks before the ECB-induced interest rate distortions accelerated on Thursday and pushed stocks lower on Friday. Financials are being hurt by the prospect of “lower for longer” again in the U.S. and weirdness from negative rates abroad. Morgan Stanley is hosting their big financials conference this week, so watch for headlines from that. The Fed meets this week, but don’t expect much action, just more talk, especially as what has come to be called the Shanghai accords continue to make Yellen afraid to act in the U.S.’s best interest. Brexit is becoming an issue for markets (I don’t think it’s as serious long-term as many pundits believe, but what I think doesn’t really matter short-term). Things feel funky out there – the sell-off Friday came on decent volume, and with conviction levels among investors near record lows, don’t expect dip-buyers to materialize right away. When volatility has been this low for this long, it can trigger big selloffs as stops are triggered and complacent investors suddenly panic. Plan for this, stay hedged, and don’t be a hero on the first leg down. SPY Trading Levels: The market is still coloring within the lines. The SPY stopped just under the 213 resistance level we mentioned in our last note after moving through the big level of 209/210. That resistance level is now support, followed by 208 then 204/205, a little at 200 and 195, then 185. Resistance: 213 has held a few times. If the markets punch through, there isn’t much above it. Positions: Long and short U.S. stocks, ETFs and options. Neutral stock exposure, slightly net short down 3%. |

Archives

March 2023

Categories |

RSS Feed

RSS Feed