|

All this time I was wasting,

Hoping you would come around I've been giving out chances every time And all you do is let me down And it's taken me this long Baby but I figured you out And you're thinking we'll be fine again, But not this time around Taylor Swift, You’re Not Sorry This letter is going to be full of weird mismatched analogies. I’m sure you’ll be ok. It goes with this weird, mismatched market we are forced to navigate. Some weirdness we’ve discussed at length: trillions of dollars of negative yielding sovereign debt, a Swiss yield curve negative out to 30 years, corporates issuing debt at 0% interest, and a Federal Reserve Board that is clearly lost and afraid of its own shadow. While central banks around the world are doing really inane things, the Fed is caught in a vicious feedback loop that it doesn’t even seem to understand it created. It gets spooked by every little downturn in the market, every reaction to a speech or meeting minutes release. In short, it’s a Hawthorne effect experiment gone bad. The Hawthorne effect (also known as the observer effect), is when individuals modify their behavior once they become aware they are being observed. When the Fed was (or at least, said they were) focused on data points from the real economy in making their rate decisions, then the market could watch those same data points and make its own determination about whether or not the macro environment favored one type of investment or another. However, ever since Greenspan started playing God with the markets and focused on asset prices in securities markets as a means to create a wealth effect and increase economic activity, the Fed has been sliding down a slippery slope of reflexivity and feedback loops. By trying to cajole markets to do its bidding without actually moving rates or following through on its statements, the Fed has become a Frankenstein’s monster of the boy who cried wolf and Schrodinger’s cat. No one believes anything a Fed official says anymore, and the Fed is both alive and dead at the same time. The annual Jackson hole retreat for Federal Reserve officials is this week, and Janet Yellen is giving a much anticipated speech. Market pundits keep writing that the speech will be eagerly parsed for signs that the Fed will raise rates sometime later this year. My view is that no matter what Chairwoman Yellen says, no one will believe her. She could stand at the podium and say “I fully believe that rate hikes are going to happen this year” and the market likely will do nothing. Why? Because Fed officials like Yellen and Dudley have lost all credibility. They’re like the little boy that cries wolf. Six months ago, the situation was different. But after so many contradictory speeches since then, the market now knows that if Yellen says she’s raising rates, and the market sells off, then they won’t raise rates, so the market will rise again. But not this time around. After wasting all this time, markets are done hoping the Fed will come around. That’s what happens when all you do is let someone down. Eventually, they figure you out. Looking so innocent, I might believe you if I didn't know Could've loved you all my life If you hadn't left me waiting in the cold And you got your share of secrets And I'm tired of being last to know And now you're asking me to listen Cause it's worked each time before Taylor Swift, You’re Not Sorry I think markets are getting tired of being left out in the cold by central banks around the world manipulating securities prices to engineer economic growth. It appears to me that this acceleration into negative rates in the past few months has been driven by a capitulation on the part of income investors who never believed that rates could get this low, so they held back, afraid of locking in (at the time) historically low rates. Then they watched with shock and horror as NIRP replaced ZIRP – and FMO (fear of missing out) kicked in. But at some point, you reach that last marginal buyer. When will that happen? Nobody knows. Central banks keep reloading and doing dumber and dumber things, and since their stupidity seems to know no bounds, I’m willing to say that I don’t know how dumb things will get before they stop. What I do know is that locking in a guaranteed loss on bonds that are held to maturity is not a good way for investors to meet their long-term liabilities. Think pension plans and insurance companies for example. Central banks are eviscerating them. How insolvent pension systems and life insurance companies can be good for the global economy is beyond my pay grade, but then again, I don’t have a Ph.D. in economics. (As an aside, I did take quite a lot of economics, including in graduate school, but quickly figured out that logic and reason had no place in the discipline. When I pointed out an obvious flaw in a professor’s work (outside of class, privately) he admitted that I was correct but that the flaw was needed to make the math work. That’s when I decided to be a history major instead.) The Fed wants markets to believe that every meeting is “live” for a rate hike, but markets know that that is simply not true. But the Fed doesn’t know that yet. Like Schrodinger’s cat, the Fed exists in a state of quantum uncertainty in which it is both alive and dead at the same time. It thinks it can move, but it can’t. And now that it knows it’s being observed, it’s stuck. Ironically, Einstein’s letter to Schrodinger in 1950 could easily be describing the state of monetary policy today. Simply replace “physicist” with “Federal Reserve Board Member”: “You are the only contemporary physicist, besides Laue, who sees that one cannot get around the assumption of reality, if only one is honest. Most of them simply do not see what sort of risky game they are playing with reality—reality as something independent of what is experimentally established. Their interpretation is, however, refuted most elegantly by your system of radioactive atom + amplifier + charge of gunpowder + cat in a box, in which the psi-function of the system contains both the cat alive and blown to bits. Nobody really doubts that the presence or absence of the cat is something independent of the act of observation.” So what’s an investor to do? I suggest building a robust portfolio. What’s a robust portfolio? A portfolio that can survive exogenous shocks to the market systems and survive. Think Jason Bourne. All sorts of bad things happen to him, and he survives. He can get shot, thrown off a bridge, chased across continents, and he survives. He’s robust. He’s the opposite of an effete central banker sipping wine in Jackson Hole this week. For the central banker, even a hint of something amiss, a tremor of market volatility, and they run away, hiding behind “uncertain market conditions” or some other such excuse. They panic. They make a bad situation worse, and they don’t know how to protect against unforeseen outcomes. They are, in the words of Nassim Taleb, fragile. Don’t be fragile. Am I saying a market crash is imminent? No. I’m saying that all the conditions for a market crash are in place. Volatility selling has pushed down implied vols to a level that will exacerbate any market downturn of about 3% or more, by my estimation. Investors desperate to generate return have taken to selling calls against their portfolios to create income, but they aren’t hedging their downside to protect against a market decline (a very low equity put-call ratio shows this). In the near-term this can work to create a false sense of calm, as investors who have sold calls can’t really sell the underlying without being left naked short, something that mutual funds are usually restricted from doing. But this low-vol environment can entice traders reaching for return to short puts as well, which can quickly become problematic and cause a cascade of selling if and when they rush to hedge their downside exposure. Even more troubling, is that this recent period of extremely low volatility is setting us up for another VAR shock, reminiscent of last summer. I wrote about this almost exactly a year ago in response to the S&P 500 diving 6% in a week. We could be in for another round of VAR shocks creating feedback loops that take markets by surprise. The conditions are all set for it. All it would take is a misinterpretation of a Fed speech, a comment from a Chinese finance ministry official about exchange rates, anything really. With 33% of the market invested in passive vehicles and ETFs viewed as a ready source of liquidity, a small market dislocation has the potential to create flash crashes in various asset classes. I’m only short ETFs, not long them, and running a market-neutral book. In short, I want my portfolio to perform like Jason Bourne. We may get beaten up, but in the end, we’ll survive. So you don't have to call anymore I won't pick up the phone This is the last straw There's nothing left to beg for And you can tell me that you're sorry But I don't believe you baby Like I did before You're not sorry, no no oh Taylor Swift, You’re Not Sorry In my last letter I laid out some charts and said that I thought there was a lot of churning going on beneath the surface of an unusually calm market. In particular, I said that I thought banks could move higher and that utilities and staples were rolling over. Well, since then, the KBE (KBW Bank ETF) is up about 5%, the XLU (Utilities ETF) is down over 3%, and the SPY (S&P 500 ETF) is up about 1%. Rising LIBOR (also discussed in the last letter) was flagged as a reason for optimism about U.S. banks (Japanese banks are cooked if this continues, but that’s a story for another day) and pessimism about bond proxies. There’s no sign that this LIBOR squeeze will abate before the October change in money market fund regulations, so don’t fight it. That said, I think it’s time to play some defense again. I’d sell half the bank position from a few weeks ago and go to cash with it. I’d stay short the utilities and staples, and pare back your tech bets. I’m still long some stocks, but fully hedged. Keep some dry powder so you can take advantage of any severe market dislocations. __________________________________________________________________________ This week’s Trading Rules:

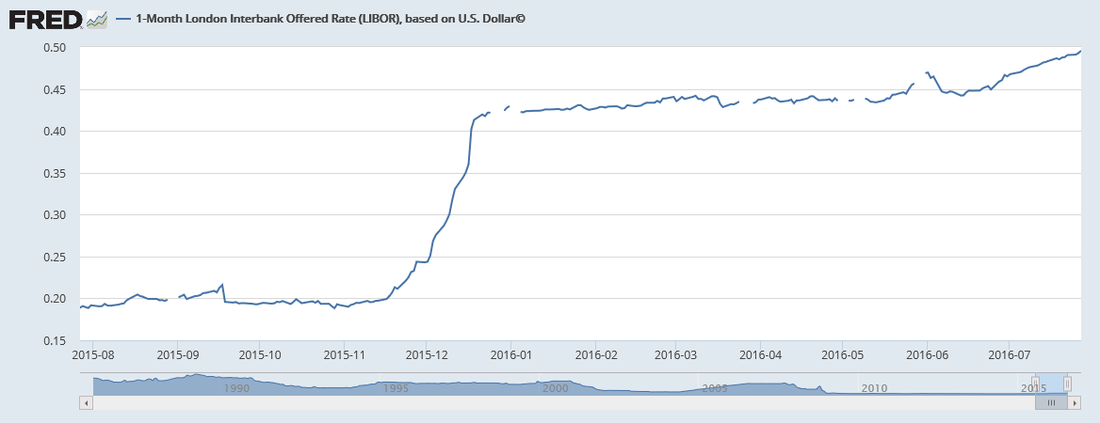

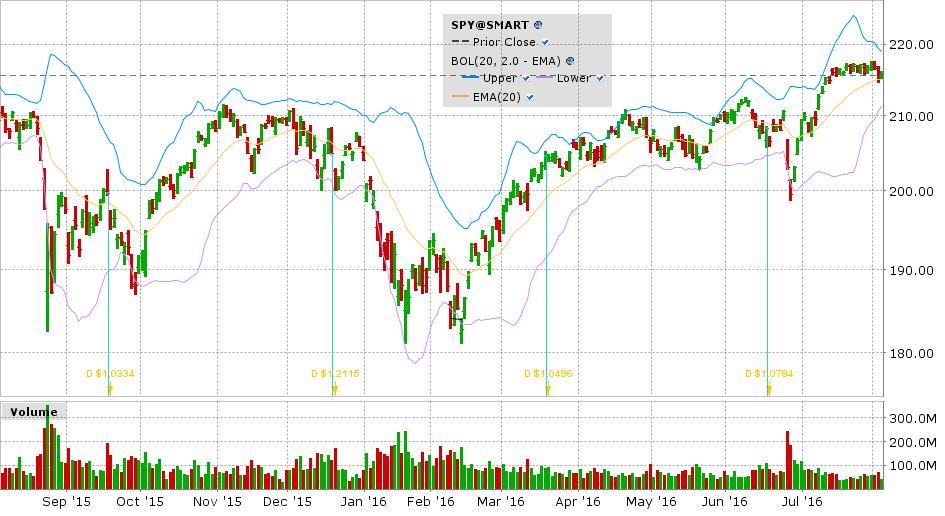

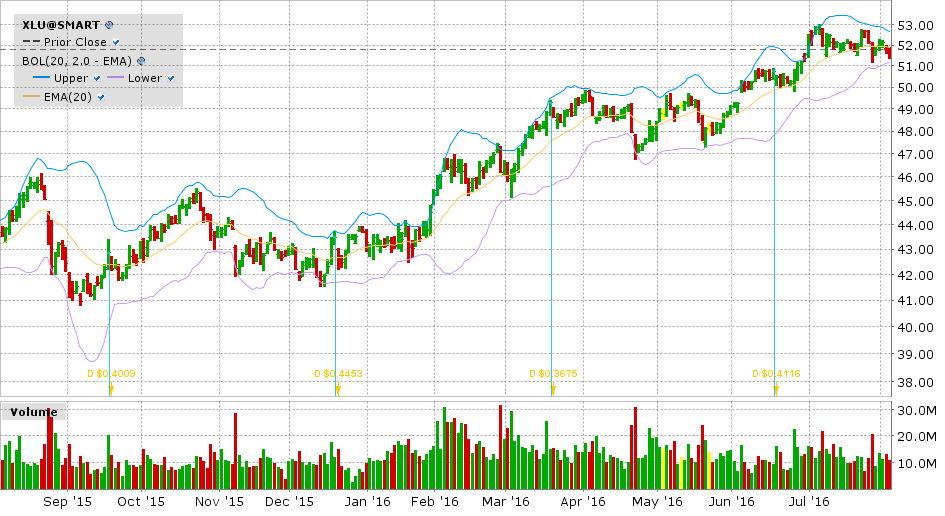

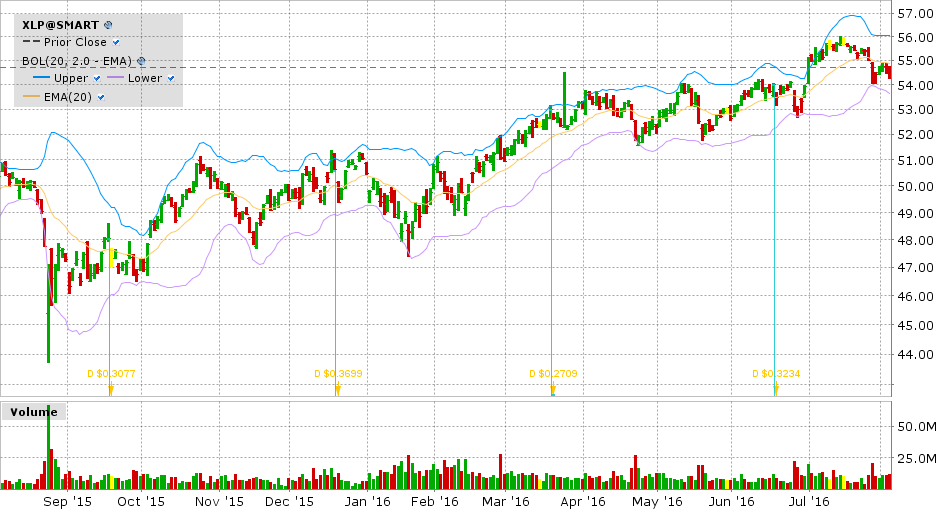

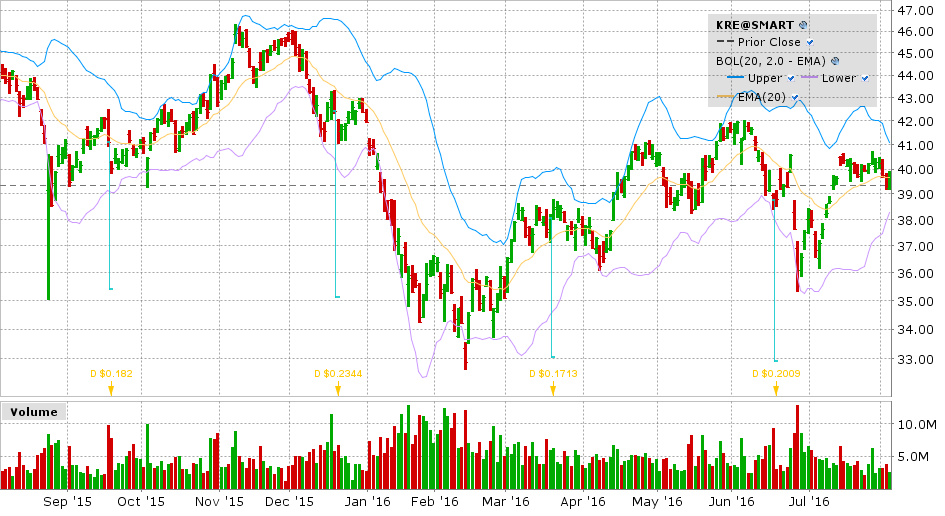

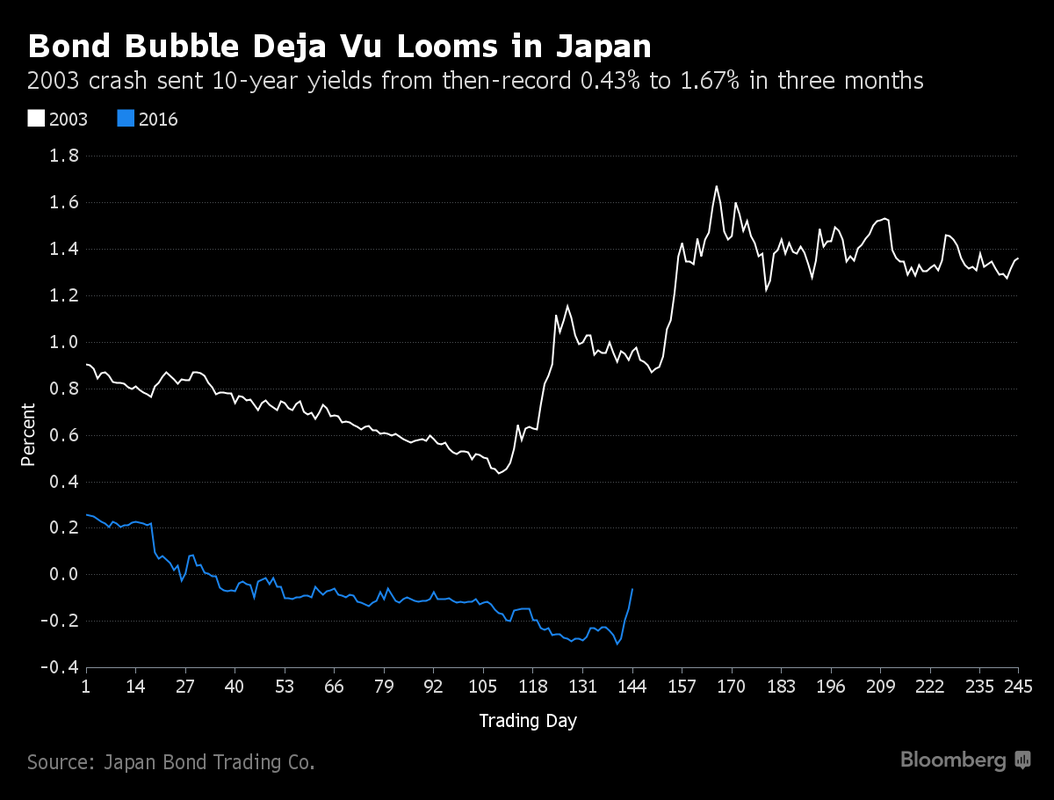

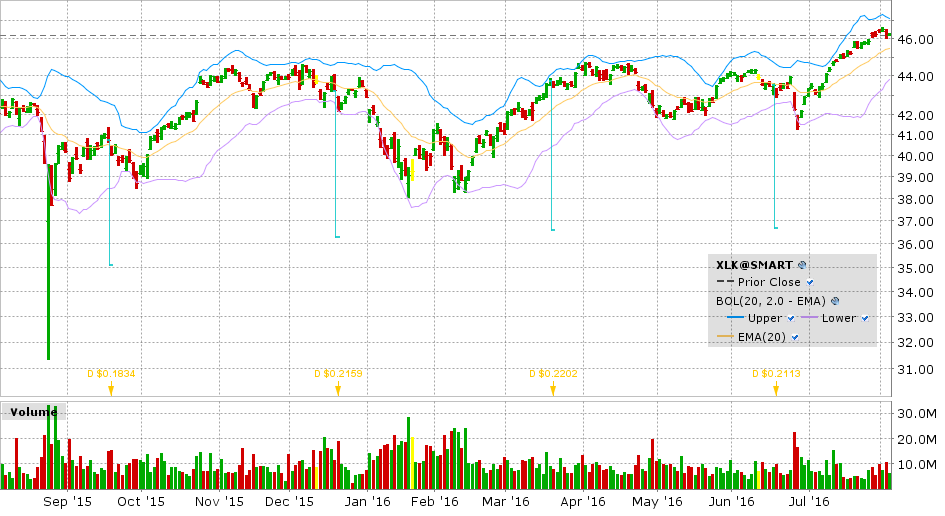

SPY Trading Levels: Resistance has moved up a little, to 219/219.50. Not much above that. Support: 217, 216, small at 212, a decent amount at 210, then 205 and 185. On a selloff of more than 1.5%, first stop will be 212. Positions: Net neutral long/short. Long U.S. Stocks, short U.S. stocks, short XLU, SPY, XLP, and BWX. August 3rd, 2016 By Jeffrey Miller, Partner, Eight Bridges Capital Management My last letter was the most forwarded letter I have written, so in case you missed it, it can be found here. You can subscribe to receive this letter in your inbox here. It is always free. Lost Boy from Neverland "Run, run, lost boy," they say to me Away from all of reality Neverland is home to lost boys like me And lost boys like me are free Ruth B, Neverland One of the advantages of a long/short hedge fund is that the portfolio manager is generally free to invest whatever way makes the most sense, without worrying about blindly benchmarking to various indices, something that often occurs when running a mutual fund. I should know – over the past 20 years, I’ve managed both mutual funds and hedge funds. Hedge fund managers are definitely freer. In a bull market, this freedom can be a hindrance, as my natural inclination is to never be 100% net long, but to hedge a bit in case the unknown macro event decides to wreak havoc with the markets. But when markets are frothy, and smart investors are lost, its nice to be free to hedge, raise cash, and just wait. Because right now the reality of financial markets is something that many big investors are saying to run away from. For example, in just the past week: Bill Gross: “I don’t like bonds; I don’t like most stocks; I don’t like private equity. Real assets such as land, gold and tangible plant and equipment at a discount are favored asset categories.” Jeffrey Gundlach: “The artist Christopher Wool has a word painting, 'Sell the house, sell the car, sell the kids.' That’s exactly how I feel – sell everything. Nothing here looks good,” Gundlach said in a telephone interview with Reuters. "The stock markets should be down massively but investors seem to have been hypnotized that nothing can go wrong." Some other strange things have been happening in financial markets lately, and many of them contradict one another. For example, the S&P 500 closed higher for 5 months in a row when it finished in the green for July. This has happened 23 other times since 1950. In all the other 23 times, the market was higher 12 months later. Buy buy buy! But then you have the fact that the market traded within a 1.04% range for the 11 days ending August 1st. What makes this extremely tight trading range really unusual is that it occurred exactly when over 70% of the S&P 500 reported earnings, which is when stocks are usually their most volatile. Maybe this is what is spooking the professionals so much – they see lots of insane pricing in bond markets and bond proxies in the stock markets, but the overall market doesn’t move. They’re lost, but they’re stuck being long in most cases. It’s nice to be a lost boy who’s free from that reality. He sprinkled me in pixie dust and told me to believe Believe in him and believe in me Together we will fly away in a cloud of green To your beautiful destiny Ruth B, Neverland When the consensus is that everything is crazy and the only prudent course is to sell all assets, I’m inclined to disagree. If bonds are about to go lower and rates higher, there will be winners and losers – the trick is to find the stocks that benefit, believe in them, and fly away in a cloud of green to your beautiful destiny. This market reminds me of early 1995. Bank stocks had rebounded from their recession lows hit in the 1990-1991 bear market, but were stuck trading under book value, as investors refused to believe that they would be able to produce sustainable earnings growth. At the same time, the Fed had begun raising rates, and the mantra at the time was don’t fight the fed – especially in financials. Fast forward 20 or so years, and you have a similar situation in the big banks in the U.S. Valuations are quite reasonable, but the stocks are stuck in a trading range, as investors debate whether or not they can generate sustainable earnings growth in the face of ultra-low rates. Unlike 1995, this time around investors clearly understand that banks do better in a higher-rate environment, and the “don’t fight the Fed” trade today will manifest itself in other sectors like bonds, utilities, and staples. Banks have started moving higher, not because Fed Funds are moving up, but because LIBOR has. Take a look at the chart below of 1-month LIBOR, and you’ll see that it spiked up in December, when fears about European banks introduced risk back into the system, and again in the past few weeks, once again on European bank capital worries. This is nirvana for U.S. banks, as most price their loans not off of Fed Funds, but off of LIBOR. If LIBOR is moving up on worries about European banks, U.S. banks benefit. If this continues, earnings for U.S. banks could surprise on the upside. Just like 1995 and 1996. 1 Month LIBOR 7/27/2015 to 7/27/2016. Source: St Louis Federal Reserve  Looking at a chart of the S&P 500 today is like looking at the ocean at low tide – it appears calm, but beneath the surface there is a lot of churning going on. If this churning continues, we could see a leadership change in the U.S. stock market, from defensive sectors to those that benefit from economic growth and higher rates. I think we are on the cusp of such a change. So sprinkle on a little pixie dust and get long select banks, technology, and media stocks, and short, or at the very least avoid, bond proxies like staples and utilities. My fund has net zero stock exposure and is short international sovereign bonds via ETFs, so I’m not saying go crazy long here, just saying that even if the overall indices don’t move much, there is opportunity to pick some winners and losers for those that like me are free. I don’t usually put a lot of charts in my letters, mainly because they make it hard to read on a phone, but here a few that I think are important right now. In particular, take a look at how while the SPY is flat, the XLU and XLP are rolling over, and the KBE and XLK are moving higher. The KBE in particular has room to run, as it’s still well below its level of late last year. In addition, I have put in a chart of the Japanese 10 year bond yield today versus 2003 (when the bond crashed on a VAR delivering) and versus the German Bund a year ago. Danger ahead? If you’re long negative yielding sovereign bonds, I’d say you’re pretty lost right now. S&P 500 (SPY)  Finally done going up? Utilities (XLU)  Rolling over? Consumer Staples (XLP)  Room to run? U.S. Regional Banks (KRE)  Japanese 10 year Bond Crash: 2003 vs Today:  Japanese 10 year Bonds vs. German 10 year Bonds: Will History Repeat Itself?  Tech Breaking Out? SPDR Tech ETF (XLK):  Charts courtesy of Interactive Brokers, LLC and Bloomberg

__________________________________________________________________________ This week’s Trading Rules:

In my June 24th, 2016 letter, I wrote: “The broader market has been performing worse than the S&P 500, as utilities and staples hold up the index. Tech and financials have been especially weak lately. I’d go shopping there for bargains if you have a time frame longer than a week. Financials are being hurt by the prospect of “lower for longer” again in the U.S. and weirdness from negative rates abroad. Tech is being hurt by weak global growth outlooks, but the best businesses will be fine, especially those with a U.S. focus.” Since then, tech and financials have done well, and utilities and staples have stalled out. I’d stick with the trade. SPY Trading Levels: Resistance has been set by the top end of the tight trading range of the past 2 weeks. Lots of resistance at 216.50/217. Not a lot above that. Support: small at 214/214/50, a decent amount at 210, then 205, 200, and 185. Positions: Net neutral long/short. Long U.S. Stocks, short U.S. stocks, XLU, SPY, XLP, BWX. Miller’s Market Musings is a free bi-weekly market commentary written by Jeffrey Miller, who has been managing money through various market environments for over 20 years. You can subscribe here. If you no longer wish to receive this letter, simply hit reply and put “Remove” in the subject line. Prior posts can be found at www.millersmusings.com. |

Archives

March 2023

Categories |

RSS Feed

RSS Feed